Hi folks,

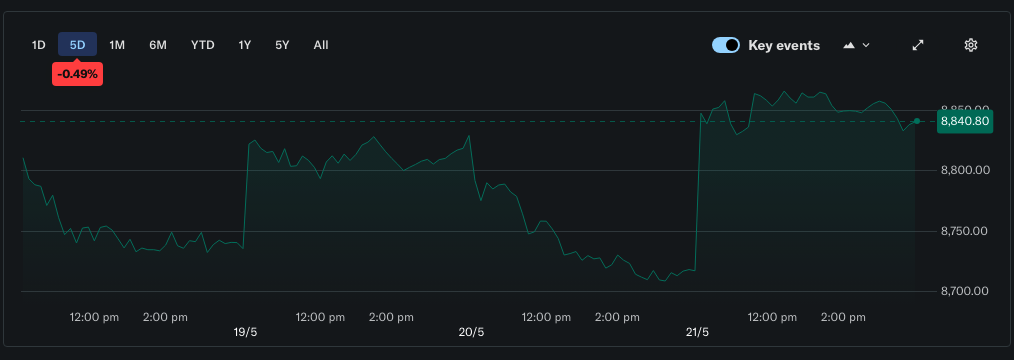

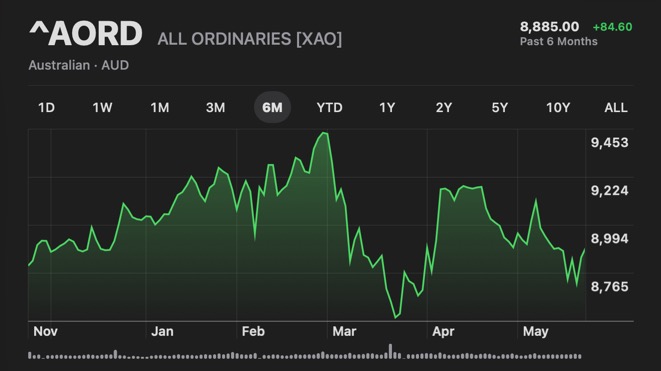

Australian markets endured a volatile week, but looks like it’s actually ending in positive territory.

It’s still a long way down since the end of February, though.

US stocks were also slightly up over the five-day period. Rising inflation concerns drove bond yields higher, but the market continues to push onwards regardless.

So, let’s get into my weekly updates and see where we are at.

All the Best,

Cam

QAV MYTH KILLERS

Microsoft 1999 – Great Business, Terrible Investment

“Microsoft sitting at such a low PE was crazy” – some guy on reddit.

From time to time during the week, I read some of the investing forums on Reddit, and one of the recurring ideas I see, surprisingly enough, particularly on the value investing subreddit, is that people are stupid and don’t understand value investing if they’re ignoring the MAG 7 stocks.

For anyone that’s new to investing or the American market, those are the companies that are currently publicly listed and at the center of the AI boom: Apple, Microsoft, Google, Amazon, NVIDIA, Meta, and Tesla.

They’ve had incredible success in terms of their stock price in the last few years, driven primarily by all of the expectations that AI is going to take over everything and they will be somewhere in the middle of it.

And while I have high hopes for AI and do believe there’s a fairly high chance that it will continue to develop and will be an incredible chapter in human history, I also remember what happened in 1999.

I was actually working at Microsoft in 1999.

We were on top of the world. Bill Gates was still CEO, most people were accessing the internet on our tech, Windows 98 Second Edition was… okay, so that sucked. But Windows 2000 was just around the corner… we were making serious cash.

On the last trading day of 1999, Microsoft closed at $35.75 a share.

At the time, they were the most valuable company in the world.

Windows ran on almost every PC on the planet.

Microsoft Office was printing money.

The internet was being built on Windows servers.

If you told an investor in December 1999 that Microsoft would dominate computing for the next two decades, most of them would have agreed.

Sure, there was some competition from Sun Microsystems and Oracle and IBM, but Microsoft was in a very strong position.

And if you’d bought 1,000 shares of Microsoft that day for $35,750, you would have waited until 2016 to break even on that price, 17 years to get back to zero.

In those 17 years, Microsoft AS A BUSINESS didn’t stagnate.

They did nothing wrong.

They quadrupled revenue from roughly $23 billion in fiscal year 2000 to nearly $87 billion by fiscal year 2014.

They paid out tens of billions of dollars in dividends.

They were profitable every single quarter for almost the entire period.

By any business measure, they were one of the great corporate success stories of the modern era.

But the stock did nothing.

Sure, you would have collected dividends, and with those reinvested, you would have done a little bit better than nothing.

But over 17 years, you would have made a low single-digit return by buying shares in the world’s most successful software business, while the broader market doubled and tripled around you.

Your capital did nothing.

Why?

This is the bit most retail investors never learn until it’s too late.

In 1999, Microsoft’s price-to-earnings ratio was 75.

The PE ratio is the simplest valuation tool there is.

You take the share price and divide it by the company’s earnings per share.

That number tells you how many years of current earnings you’re paying for in advance.

A PE of 15 means you’re paying about 15 years of current profits to own a share.

A PE of 75 means you’re paying 75 years.

The long-run average PE for the S&P 500 is around 15 to 18.

Microsoft was trading at four times that.

What does a 75 PE actually mean for an investor?

It means you’re betting that profits will grow enormously fast for a very long time just to bring the multiple back to something normal.

And that’s exactly what happened.

Profits grew, dividends were paid, the business was excellent.

But the multiple compressed from 75 in 1999 down to around 12 by the early 2010s.

Let’s think about it in terms of the coffee shop analogy that Tony likes to use.

Imagine there’s a great cafe in your suburb that is absolutely killing it.

Lines around the corner every weekend and every weekday.

Rave reviews for their coffee, their banana bread is out of sight, their muffins are bouncy, the staff have all studied Will Guidara’s “Unreasonable Hospitality” cover-to-cover.

People travel from around the world just for a sip of their single origin cold brew.

It’s doing so well that it’s making a million dollars profit a year.

I don’t know if there are any cafes in the world that make that kind of profit, but just go with me here.

And let’s say you’re offered a chance to buy the business and the going price that the owners are asking for is $75 million.

Now you’d have to ask yourself, what are the chances that I’m going to get that money back?

Sure, it’s a great cafe today, and it will probably be a great cafe tomorrow, but will we be able to hold that reputation and that position for 75 years in order for me to just get my money back, let alone make a profit on it.

Now let’s look at the Magnificent Seven in 2026.

Apple has a PE around 37, Microsoft 25, Google 28, Meta 18, Amazon 30, Nvidia 45, Tesla 355!!!!

Tesla is in a category of its own. At 355, Tesla buyers today are paying nearly five times what Microsoft buyers paid in 1999 – and we already know how that one ended.

Even the other six are all well above the historical market average.

The bullish case for each one rests on the same bet that Microsoft buyers made in 1999.

The company will keep growing fast enough for long enough to justify the price you’re paying today.

I’m not saying that any of these stocks will go sideways for 17 years.

They might double from here, they might do better than that, or they might not.

The point is that the principle that destroyed Microsoft buyers for nearly two decades is exactly the same one operating on Mag 7 buyers today.

If you pay a premium price for premium growth you need that growth to keep showing up year after year, decade after decade, and the multiple still has to hold.

Cisco was the king of the internet build-out in 1999.

Their stock peaked at $80 in March 2000.

It didn’t see that price again for more than two decades.

Intel was untouchable.

Their 2000 peak was around $75.

They’ve spent most of the past 25 years well below it.

Warren Buffett has written about the Nifty Fifty of the early 1970s, the blue-chip MAG 7 equivalents of their day, that ate a decade for buyers who paid the going rate.

Every era has its obvious winners.

A few keep winning.

Almost none of them keep winning at the price the crowd is willing to pay.

And you only know which ones are going to win in hindsight.

The QAV process that Tony developed doesn’t ask, is this a great business.

It asks, is this a great business at a sensible price?

Those are different questions.

The first one would have put you into Microsoft in 1999.

The second would have kept you out.

A high QAV score requires both quality and value.

The checklist combines a quality screen, good return on equity, clean balance sheet, real cash flow, a sound business model, with a value screen, a sensible price to operating cash flow ratio, margin of safety against intrinsic value.

Stocks at a PE of 75 don’t get onto the buy list.

Stocks at a PE of 40 usually don’t either.

The rules force you to ask what you’re actually paying, not just whether the company is famous.

A few months ago I wrote a piece called “Invest in MASS, not GAS”.

QAV invests in companies with real mass, i.e. quality businesses generating real cash flow at reasonable prices, and avoids the gas giants whose stock prices are built almost entirely on predictions of future dominance.

Microsoft in 1999 was the largest, brightest, most successful gas cloud in the history of capital markets.

The mass was real.

The business kept compounding, but the price you paid for it was almost entirely gas.

Keep in mind that the most vocal advocates for buying the Mag 7 are people that have already invested in them and therefore have a vested interest in their continued price appreciation.

Maybe all of those businesses will continue to boom for 10 more years.

Maybe only some of them will.

Maybe none of them will.

Nobody really knows.

What I do know is I’m not going to wait 75 years for my cafe to break even.

STOCK ANALYSIS OF THE WEEK

I added a couple of stocks to the Light portfolios this week and you can see my Light posts here.

I also added something to the U.S. Light portfolio this week. U.S. Light and Club members can read about it here.

On the full Australian podcast this week, Tony did a deep dive on TIP. See the podcast link down below if you want to listen to his analysis.

BUY LIST

Each week, we produce a buy list based on our value investing system that we share with our QAV Club members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

QAV Value Investing Buy List (AU) 2026-05-15

Below is a link to the US list for this week (available exclusively to our U.S. Club members):

QAV Value Investing Buy List 2026-05-17

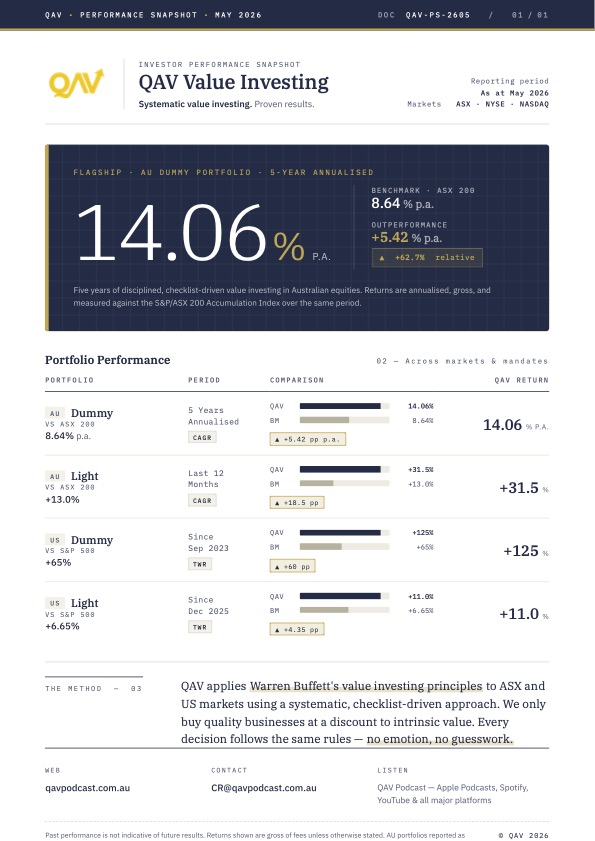

PORTFOLIO PERFORMANCE

We compare our performance to what we think is the most relevant benchmark (SPDR 200 in Australia, S&P500 in the USA), but if you’re new to investing, these comparisons might not mean much. Instead, you can compare our performance to the top-performing Super Funds in Australia and see why an amateur active investor (who has a system to follow) can out-perform most of the “professionals”.

We publish a fresh performance snapshot once a month. Weekly noise doesn’t tell you much in a value-investing system — what matters is the trend.

May 2026 performance snapshot.

Become a QAV Light Member today and start your investing on the right track

If you want to find out what we’re trading in QAV Light each week, sign up to become a member. You’ll get an email from me every Monday letting you know what we’re buying and selling in that portfolio. You can choose to copy our trades or not. It’s the easiest way to start your rules-based investing career… and you don’t even need to know the rules. I’ll follow the rules for you. It’s a good first step to eventually becoming a QAV Club member and learning how to run the system by yourself.

QAV LIGHT: We know where to drop your line.

(Note: Americans interested in joining QAV Light or Club please go here instead.)

THIS WEEK’S EPISODES

The Gas That Moves the World: BWLP – QAV America #53

STOCK NEWS AND UPDATES

COMMODITIES

This week the big changes to commodities were the following:

| Commodity | Status |

|---|---|

| Iron Ore | BUY |

| Gold (USD) | JOSEPHINE |

| LNG | JOSEPHINE |

| Wheat | BUY |

DISCLOSURE

Please review our trading and disclosure policy.

SIGNING OFF

Another week over, QAV crew!

Remember, while everyone else is chasing momentum and hot tips, we’re quietly building wealth through systematic value investing and letting compound interest work its magic.

SSDD!

- Cam

That’s it for the week!

QAV A GOOD SHAREMARKET!

Got a question? info@qavamerica.com