Hi folks,

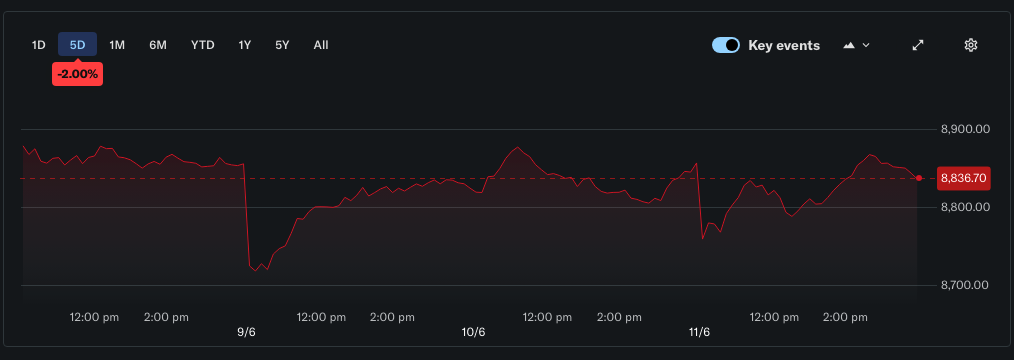

The All Ordinaries experienced significant volatility over the past five days, amid spiking oil prices, dramatic swings were primarily driven by escalating tensions in the Middle East, though the market found some relief toward the end of the period on hopes for a potential ceasefire and softer inflation data that reduced expectations for further RBA rate hikes. It seems to be up today as Trump TACO’d yet again.

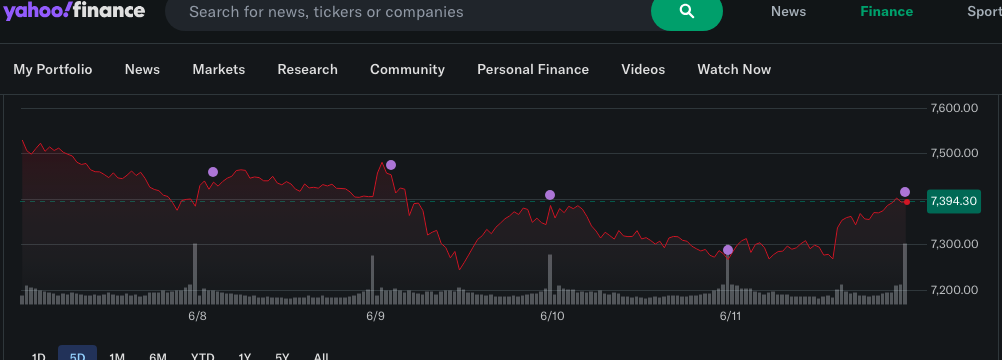

US markets also endured a volatile week, with the S&P 500 sliding from around 7,500 to a low near 7,250 mid-week before recovering to close at approximately 7,394 yesterday. The market’s recovery was driven by AI stocks swinging back upward, helping Wall Street claw back some of the week’s earlier losses.

So, let’s get into my weekly updates and see where we are at.

All the Best,

Cam

QAV MYTH KILLERS

The Fast and the Strong

“Don’t fight the tape.”

“Make the trend your friend.”

“Cut your losses and let your winners run.”

All these Wall Street maxims mean the same thing — bet on price momentum. Of all the beliefs on Wall Street, price momentum makes efficient market theorists howl the loudest. The defining principle of their theory is that you cannot use past prices to predict future prices. A stock may triple in a year, but according to efficient market theory, that will not affect next year…. Conversely, another school of thought says you should buy stocks that have been most battered by the market. This is the argument of Wall Street’s bottom fishers, who use absolute price change as their guide, buying issues after they’ve done poorly. Let’s see who is right.

I’m quoting from Chapter 15 of “WHAT WORKS ON WALL STREET” by James O’Shaughnessy.

He did some analysis on the 50 stocks with the best and the worst 1-year price changes from both the All Stocks and the Large Stocks universes to see which cohort performed the best in the following year, using December 31, 1951 as the starting date – and holding them until the end of 1994. That’s a very long, 43-year game of “buy and hold”.

So what happened?

The stocks from the “best” list performed pretty well – a compound return of 14.45 percent a year. They were, however, highly volatile, and he warns that not many investors would have the stomach for that kind of wild ride.

How about the stocks from the “worst” list? Well they had a compound return of… 2.54 percent a year.

His conclusion?

“Runyon’s quote is apt. Winners continue to win and losers continue to lose.”

The same $10,000, over the same 43 years, became $3,310,255 in the winners and $29,351 in the losers.

And while, yes, this version of this book uses 1951-1994 US data, later editions and modern momentum research confirm the pattern still holds.

Runyon Who?

If you aren’t too sure who “Runyon” was – Damon Runyon was the American short-story writer best known for the Broadway tales that became the musical Guys and Dolls. He wrote stories celebrating the world of Broadway in New York City that grew out of the Prohibition era – gamblers, hustlers and showgirls, who spoke distinctive wisecracking slang where gangsters had colourful names like “Nathan Detroit”, “Harry the Horse”, “Good Time Charley”.

The line O’Shaughnessy uses is Runyon’s most quoted: “It may be that the race is not always to the swift, nor the battle to the strong, but that’s the way to bet.”

It’s itself a riff on Ecclesiastes (“the race is not to the swift, nor the battle to the strong…”). Runyon’s twist is the punchline: sure, upsets happen, but if you’re betting, he would back the fast and the strong. So do we. We just refuse to pay full price for them.

Isn’t this like the DOGS of the DOW?

Long-time listeners might recall us discussing the “Dogs of the Dow” concept over the years. It’s the same same but different. The Dogs of the Dow is an investment strategy popularised by Michael B. O’Higgins in a 1991 book which proposes that an investor annually select for investment the ten stocks listed on the Dow Jones Industrial Average whose dividend is the highest fraction of their price, i.e. stocks with the highest dividend yield. So they tend to be high-yielding stocks whose share price has been battered over the last twelve months. This is the big distinction with the O’Shaughnessy experiment, which didn’t take into account dividend yield (he looks at that in a different chapter).

Similar Dogs experiments have been done annually in Australia. The strategy tends to perform okay – overall it beats the index, which is better than most active fund managers – but it doesn’t perform as well as QAV over the long-term.

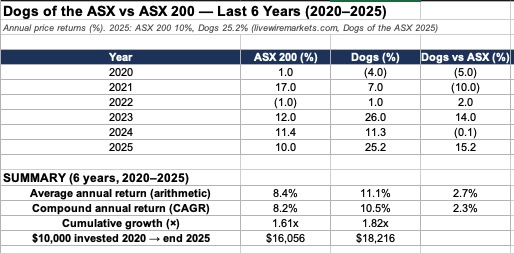

From the results provided by the annual updates from Hugh Dive (Atlas Funds Management) over the 11 years 2014-2024:

The ASX200 returned 7.5% p.a. and the Dogs returned 10.3% Compound (CAGR). So it outperformed but nowhere near the double market outperformance we strive for.

As a better direct comparison to QAV:

For the calendar years 2020 – 2025, the Dogs returned 10.5% versus the ASX200 8.2% CAGR.

The QAV Dummy Portfolio returned 16.8%.

How does this apply to the QAV strategy?

We like investing in winners of a particular variety – cheap winners. We try to invest in companies that have a history of generating cold, hard cash, which we take as a signal of a healthy business and strong management. But, of course, we only invest in those companies when we can buy the stock at a discount to their intrinsic valuation. Why? Because valuing a stock is a bit of a dark art. There are lots of variables that we can’t be completely aware of, market nuances that aren’t obvious, industry trends that we don’t appreciate, things like that. So we try to build in a moat around our investments, which means that even if we get things a bit wrong, we should still come out on top – most of the time. It’s a security measure.

So the Dogs aren’t “buy losers.” They’re “buy quality at a temporary discount.” That’s a value strategy wearing a contrarian costume – and it’s exactly why O’Shaughnessy’s own work shows high dividend yield works among large stocks while worst price performers fail across all stocks. No contradiction. The two findings are best friends.

We don’t buy losers hoping they bounce, and don’t chase winners blindly off a cliff. Buy quality businesses that are winning and still cheap.

Here’s the twist. O’Shaughnessy is watching share prices. We’re watching businesses. We don’t buy a stock because its price is climbing – we buy a cheap, quality company and then let our rules do the sorting. The sell discipline cuts the losers before they become falling knives, and lets the winners run until the trend breaks. We end up holding winners and dumping losers – the exact pattern O’Shaughnessy rewards – but we get there through rules, not by chasing a chart. No tree grows to the sky, as Tony says. We just let our system tell us when it’s stopped growing.

STOCK ANALYSIS OF THE WEEK

I added a couple of stocks to the Light portfolios this week and you can see my Light posts here.

I also added something to the U.S. Light portfolio this week. U.S. Light and Club members can read about it here.

On the full Australian podcast this week, we did an interview with Tobias Carlisle, so there wasn’t a pulled pork.

BUY LIST

Each week, we produce a buy list based on our value investing system that we share with our QAV Club members. The intended primary purpose of this buy list is for club members to use as a reference for comparing their own buy list. In theory, all of our buy lists should look pretty similar each week.

QAV Value Investing Buy List (AU) 2026-06-05

Below is a link to the US list for this week (available exclusively to our U.S. Club members):

QAV Value Investing Buy List 2026-06-07

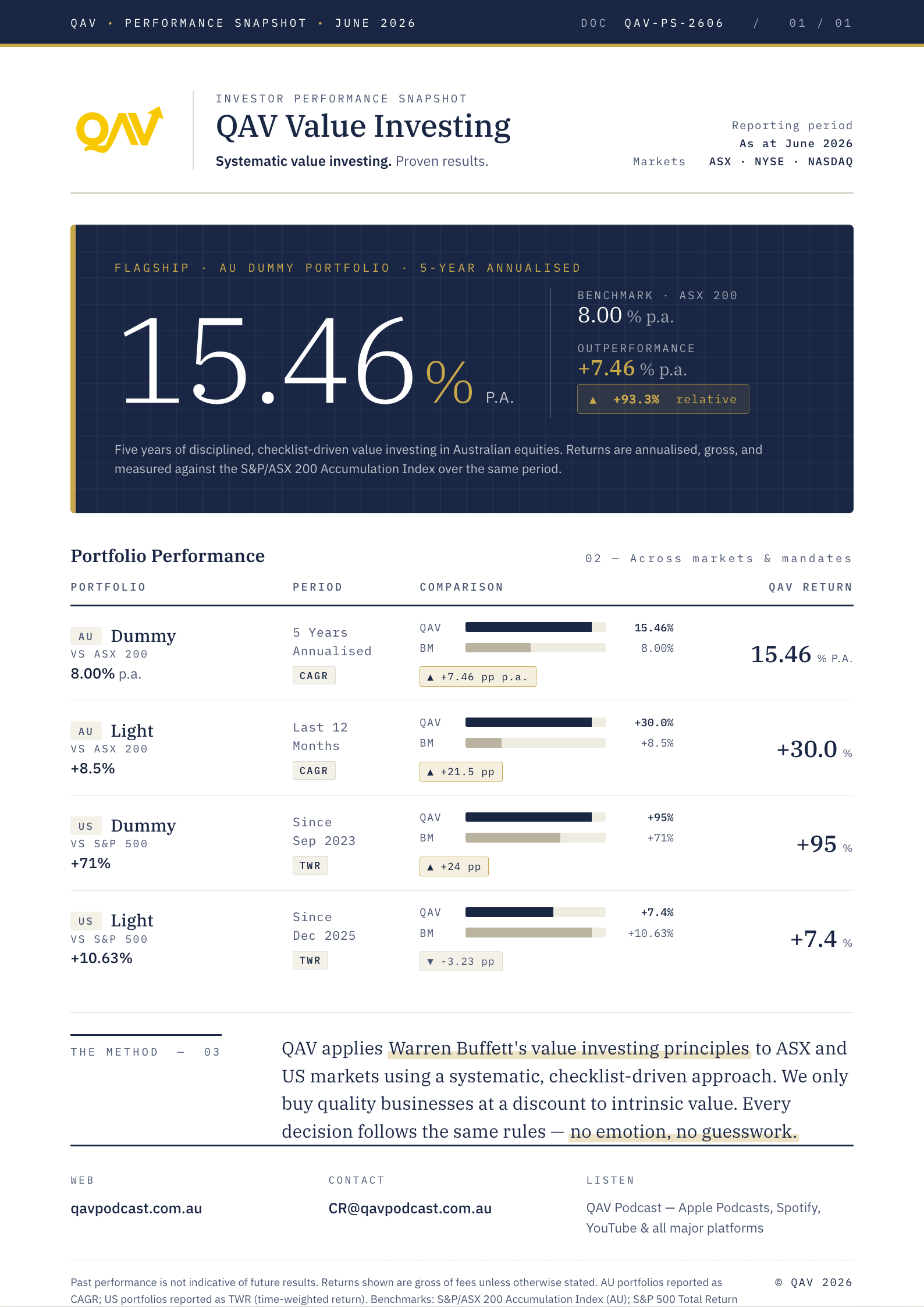

PORTFOLIO PERFORMANCE

We compare our performance to what we think is the most relevant benchmark (SPDR 200 in Australia, S&P500 in the USA), but if you’re new to investing, these comparisons might not mean much. Instead, you can compare our performance to the top-performing Super Funds in Australia and see why an amateur active investor (who has a system to follow) can out-perform most of the “professionals”.

We publish a fresh performance snapshot once a month. Weekly noise doesn’t tell you much in a value-investing system — what matters is the trend.

June 2026 performance snapshot.

Trades this week

Australian portfolios: No trades this week.

American portfolios: No trades this week.

Become a QAV Light Member today and start your investing on the right track

If you want to find out what we’re trading in QAV Light each week, sign up to become a member. You’ll get an email from me every Monday letting you know what we’re buying and selling in that portfolio. You can choose to copy our trades or not. It’s the easiest way to start your rules-based investing career… and you don’t even need to know the rules. I’ll follow the rules for you. It’s a good first step to eventually becoming a QAV Club member and learning how to run the system by yourself.

QAV LIGHT: Same destination. You choose where you sit.

(Note: Americans interested in joining QAV Light or Club please go here instead.)

THIS WEEK’S EPISODES

Tobias Carlisle Soldier of Fortune: QAV AU #923

Tobias Carlisle, Soldier Of Fortune: QAV America #56

STOCK NEWS AND UPDATES

COMMODITIES

This week the big changes to commodities were the following:

| Commodity | Status |

|---|---|

| Iron Ore | JOSEPHINE |

| Crude Oil | SELL |

| Copper | JOSEPHINE |

| Aluminium | JOSEPHINE |

| Magnesium | JOSEPHINE |

| Nickel | JOSEPHINE |

| Lithium | JOSEPHINE |

DISCLOSURE

Please review our trading and disclosure policy.

SIGNING OFF

That’s a wrap on another week of QAV. Remember to ignore the noise and focus on maintaining your own discipline. Eat healthy, get some exercise, remember to touch grass, and don’t let the bastards get you down.

SSDD!

(Stay Safe, Don’t Die)

- Cam

That’s it for the week!

QAV A GOOD SHAREMARKET!

Got a question? info@qavamerica.com