Episode Overview

This week we dive into Korea Electric Power (KEP), a deep-value, government-linked Korean utility that has quietly swung from crisis-level losses to massive operating cash flow. We explore the company’s unusual history stretching back to a royal electrification project in the 1890s, its modern political entanglement with tariff controls, its nuclear-heavy energy mix, and why the market may be mispricing a regulated monopoly with a price-to-operating-cash-flow ratio of 1.5. We also cover the recent sell of VSAT on a 3PTL rule, the psychology of Reddit outrage at PCG, and the broader role utilities play in an AI-powered future where electricity becomes the new picks and shovels.

Timestamps

00:00 – Opening chatter, Reddit outrage.

00:01:15 – VSAT sell rule triggered

00:02:00 – Introducing this week’s pulled pork: KEP

00:22:00 – Portfolio philosophy: buy deep value, sell by rules, ignore Reddit foam

00:23:00 – Final wrap-up and sign-off

Transcription

Cameron: Welcome back to QAV America, Tony, episode 29. Uh, how are you?

Tony Kynaston: well, thank you. Yep. All

Cameron: I tell you what, the folks on Reddit on the value investing sub Reddit did not like my PCG uh, Paul Pork. Last week I did a summary of it for Reddit. Oh, the hate for PCG

Tony Kynaston: bet.

Cameron: was, so, it was great. They had,

Tony Kynaston: did

Cameron: mean, there’s so much hate.

Tony Kynaston: with Love?

Cameron: I did, I called it Leading With Love.

Yeah, yeah. Uh, and manslaughter. I, um,

Tony Kynaston: What? Oh, so PC G’s part of the hive mind on Pluribus. Now they come

Cameron: yeah, it is,

Tony Kynaston: love.

Cameron: they’re leading with love. Yeah. That should be the tagline for that show. Um, but, uh, yeah, and it was just h hilarious to me how much anger and hate came out, and I was like, Hmm.

Tony Kynaston: Well, I’m

Cameron: Sounds like a good investment.

Tony Kynaston: I.

Cameron: Well, but they weren’t talking about the manslaughter. They were just talking [00:01:00] about it being a dog of a company

Tony Kynaston: okay.

Cameron: and somebody was going on about how they diluted their shareholders when they had to pay for the fires.

And I’m like, and why do I care? Like I’m, I’m looking at it post dilution, not,

Tony Kynaston: Yeah.

Cameron: doesn’t affect me as an investor today, what happened in 2019, or whatever it was. Anyway. I did have to sell something outta the US portfolio. This week I sold Vsat. It was a three point trend line sell, and I replaced it with the company.

I’m doing a pulled pork on today. Korean Electric Power, Korea Electric Power, KEP. Kepco. One of the few times I’ve been able to actually do a pulled pork on a stock that is now in our portfolio. Because I actually had to sell something. Don’t tell me what happened to the share price for Vsat today because you just broke the Ex-Girlfriend rule on our Australian show, and uh, I don’t want you to do it again.

So, uh. The kept story. I know you’ve got furniture being delivered, so I’m gonna [00:02:00] run through this one quickly today. Uh, another power company. So last week we did PCG. This is another power company, obviously based in Korea. If you hadn’t guessed from the name another regulated monopoly like last week’s show, but this time they’re regulated monopolies in entire country, not just parts of California.

Although we know California’s pretty big. And just a heads up, KEP report their financials in Juan, KRW. Bit like posco, the steel slash energy company that we covered a while ago on a, an earlier episode, episode 12, I think I did. Posco. And they’re also a competitor to KEP as it turns out. But we’ll get into this, but when you look at the numbers in stock, EDIA, they’re all in one, so you need to do the conversion.

Uh, one USD is about 1,465 KRW, uh, what was that TV show in the eighties? Um, about a radio [00:03:00] station in the us That was it. Not, not, not the Korean one. WKRP, not KRW. Okay. The current share price at the time I’m doing this for KEP is about $16 74. They’re listed on the New York Stock Exchange, so, uh, they’re known in Korea as ion I believe.

What they actually do is, well, they’re basically the power grid for South Korea. Um, essentially they transmit, generate, transmit, and distribute electricity to almost every type of customer, from households to Samsung fabs, to shipyards, to farms. The entire market is what they look after the National Grid.

They handle virtually a hundred percent of transmission and distribution. They have about six generation subsidiaries across coal, gas, nuclear, wind, solar, you name it. [00:04:00] They produce about 60 to 70% of the electricity. There’s a handful of companies, including Costco, that uh, also generate electricity. Poco.

When we did the pulled pork on them, I mentioned as a steel company, but it turns out steel mills are effectively power plants in disguise.

Tony Kynaston: Okay.

Cameron: making steel requires an immense amount of heat and energy. And when you blast iron ore and furnaces to make steel, you produce byproduct gases, waste gas, which instead of venting the gas, they capture it and burn it in their own onsite power plants to generate electricity.

And they became so good at it that they started building standalone power plants and selling electricity back into the grid. And I think they might even be the second largest, uh, generator of electricity now. In Korea after Kepp. But uh, back, back to kep. [00:05:00] They also sell power related services. They run it and maintenance businesses around the grid.

They have a whole bucket load of overseas projects, including they own a couple of coal mines in Australia or have interest in one boutique coal that they’ve had for. 15 years and they bought another one by Long Coal Mine. But they own a bunch of stuff all over the world related to energy. But, uh, you know, last week’s show, PCG, we had great.

Well, not great. Fascinating stories about manslaughter and, uh, terrorist attacks and all sorts of stuff. Just a good story behind the founding of this company. Uh, not directly related to Kepp, but worth telling anyway. ’cause I’ve found it fascinating. The company started life in 1898 as the sole electric company.

It was a [00:06:00] royal project by King Gaji who brought together trams and electric lights into the capitol. He ruled Korea for 43 years, from 1864 to 1907, first as the last King of Joon, and then is the first emperor of the Korean Empire from 1897 until he was forced to abdicate by the Japanese in 1907. And his wife, queen Min, who posthumously honored as the Empress.

Was even more powerful than he was apparently at the time of her death. She was this canny political player who was even more powerful than him, apparently, and was roundly hated in Korea by her, by his father, as well as the Japanese that were [00:07:00] ostensibly running the country at the time. And there was a conspiracy against her.

One night agents were let into the palace by pro Japanese, Korean guards. Once inside, they beat and threatened the royal family and the occupants of the palace. As they were looking for her two women were killed mistaken for her. Um. Then they eventually located her, and I won’t give you the details, but it wasn’t nice what they did to her.

She was assassinated by these Japanese agents and then her corpse was covered in oil and set fire to, so that’s how unpopular she was. She had Aly begun negotiations with the Russian Empire to align Korea with the Russians to play ’em off against the Japanese.

Tony Kynaston: high. power prices.

Cameron: No, I don’t think there was a lot of [00:08:00] power actually getting out to people at the time. Um. The king was first crowned in 1863 at the age of 12, and as I always say on my Roman Empire shows nothing works out better for a country than making a 12-year-old emperor. You can’t go wrong with that

Tony Kynaston: Fox works well at your

Cameron: Give, oh my God, nothing.

Nothing could ever go wrong, giving complete power to, uh, a child. Never in history. Has that ever been a bad idea? So the Hung Song Electric Company, as it was known. Completed its first power plant in 1899. By the end of that year, they had launched their first streetcar service. They turned on the first electric lights in SO’S Jon, go Street, Jong yo Street, and then they continued to build a public lighting network and.

Started offering electrical services to private homes. They even built a movie theater, which could be traveled [00:09:00] to by streetcar that went through downtown Seoul. And apparently it was, uh, a marketing ploy to promote the convenience of trains and attract tram passages over the 20th century. This basically morphed through nationalization and reorganization into Kepco.

Modern corporation dates from 1961 and it’s always sort of been a political en enterprise. Really it’s all been about building a modern South Korea. It was run by Americans for decades until they were forced to sell it eventually to, uh, a Japanese company in the early part of the 20th century. But, uh, after World War ii, you know, America obviously was basically running South Korea for a very long time.

After, well before the Korean War and during, and then after the Korean War. South Korean dictatorships were basically proxies for [00:10:00] the United States. Probably still are to a large degree, although no one would wanna say that publicly. Um, the Korean government invested a ton into it, even though it. But it floated on the Korean Stock Exchange in 1989 and then on the New York Stock Exchange in 1994.

But it, it was like the Korean Development Bank and the National Pension Service. It was seen as one of the founding principles of the modern South Korea. Today the government owns just over 51% of kepco, but it’s a, a lot of what it does is still driven by government policy decisions, not just market forces.

So that’s a good and a bad thing. It has a, essentially a monopoly that’s government protected, but also as we’ll see it in recent times, it has been bleeding cash. Largely because of government policies, fuel costs spiked after Russian’s invasion of Ukraine, but the government was [00:11:00] slow to let retail tariffs rise, so they were selling electricity at cost for a couple of years there, racked up huge losses and debts.

Which the, uh, market didn’t react very positively to, but that did start to turn. So in 2023, they were allowed to do tariff increases, plus they had a policy swing back in favor of nuclear shorter maintenance outages. New reactors were coming online, and that’s driven a big rebound in profitability. Q3, 2025.

They reported an operating profit of about 11 and a half trillion, one and net profit of around 7.3 trillion one for the first nine months. Uh uh can you quickly divide those by one and a half thousand, Tony?

Tony Kynaston: sorry.

Cameron: Okay. The credit rating with fit is now AA minus and gives it a stable outlook, so. They’ve had [00:12:00] a turnaround, but you know, there’s, there’s some issues there with the government’s level of control over it that I think the share market is, uh, being cautious about.

But at the end of the day, their economic engine is pretty simple. They basically just sell a gigantic volume of generated electricity and regulated tariffs as long as they keep their operating costs under control. It should be easy money for a company like this. And, you know, they do generate a lot of cash and the uh, price to cash flow will blow your mind when I get to that in a second.

But, like, like a good business, good, good sort of value investing business. It’s boring.

Tony Kynaston: Mm,

Cameron: It’s just like we did, like the PCG last week. All they’re doing is generating and selling energy.

Tony Kynaston: try not to kill people.

Cameron: Try not to kill people. Yes. And try not to have, yeah. [00:13:00] They’re leading with love and Korea. They’re going gangam style on Korean energy. It’s the only Korean reference I really know.

Tony Kynaston: happy to see, happy to see this on the buy list when, when you said you were talking about it, because of that fact. It’s a, a regulated utility. It’s a great value stock.

Cameron: Not just on the buy list, but at the top of the buy list, which is why I added it to our portfolio this week. Yeah, they’ve got a monopoly status, so the, but as I said, good and bad can come with this level of government control that they have. But they’ve got a, a quite a large nuclear fleet, which has some structural advantage versus pure fossil fuels.

The government has a 2038 plan, which explicitly increases nuclear share of the mix and slashes coal. And as we know, I mean, I dunno really what South Korea’s doing from an AI perspective and generating electricity for AI data centers, but I’m sure they’re [00:14:00] doing something. I’m sure Samsung has got a major robotics and AI plan.

Uh, as long, I know that from looking at what China is doing in robotics and ai, that the car companies like Tesla is in the us, the Chinese car companies are all over robotics and ai. I’m sure the. South Korean car and technology companies aren’t being left behind in that space as well. So these guys will probably have to provide all of the electricity and power to all of the robot and AI farms that’ll get built in South Korea in the next 10 years.

Tony Kynaston: Which is the

Cameron: Uh,

Tony Kynaston: typical sale picks and shovels in a gold brush scenario, isn’t it?

Cameron: exactly. Yeah. Who cares which AI company wins? Uh, as long as you are. Yeah, as long as you are providing the electricity for all of them. But the market is still discounting it and, and possibly for good reasons. Uh, investors are looking at recent losses. You know, they could be worried about tariff, [00:15:00] populism, they could be worrying about the W and its weaknesses.

They can see climate and transition risk from coal to gas assets. That may need to be retired early, et cetera, et cetera, et cetera. Climate, there are some climate lawsuits against kepco farmers and youth groups are apparently suing them over climate related crop damage and climate related impacts on quality of life and all of that kind of stuff.

So it may be a liability wedge moving forwards. Uh, but you know, we don’t try and forecast the future. Our job is to look at the numbers and let me take you through the numbers. Are you sitting down price to operate in cash flow? 1.52. Tony.

Tony Kynaston: Fantastic.

Cameron: You are paying about one and a half dollars of market cap for every dollar of operating cash flow for a, for a regulated monopoly in South Korea.

So I mean, either the market [00:16:00] thinks that this level of cash flow is unsustainable high, or it’s heavily discounting political and transition risk.

Tony Kynaston: well, as we spoke about on the Australian show, it could, This company may have some big CapEx requirements coming up too. So the cash may need to be used. It’s building nuclear power plants, almost certainly, but um, at the moment, throwing off lots of cash.

Cameron: Yeah, the Petrovsky F score is eight out of nine.

Tony Kynaston: Hmm.

Cameron: Which is one of the highest, I think, or the highest, equal, highest we’ve ever seen. It’s ticking nearly every financial health improvement box right now. Margins improving leverage, stabilizing cash flow strengthening after a period of pain, so you know, at least the F score.

Believes that Kepco is a healthy recovering business, not a zombie utility. Somebody, uh, in Reddit, when I response to the PCG said, utilities [00:17:00] never compound.

Tony Kynaston: Utilities never come. What does that mean? They don’t grow.

Cameron: I guess you’re not gonna get double bagger out of utilities or something, but like, yeah, whatever dude,

Tony Kynaston: Okay. They kind of do, and if you

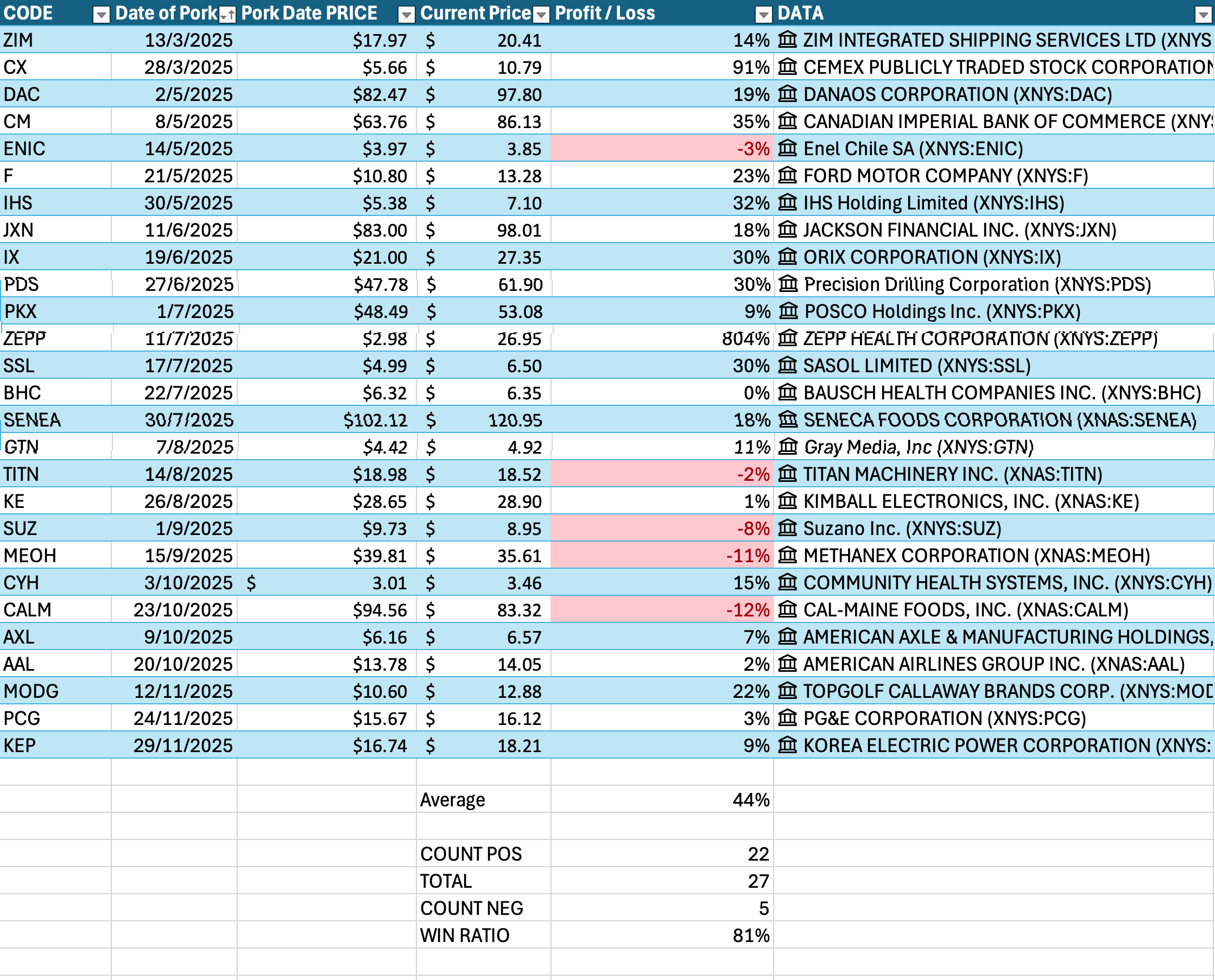

Cameron: somebody said. Somebody said, uh, this is a stock I’m more likely to short than buy. I was like, well, why don’t you do that? And we’ll compare notes in a couple of years. I don’t know. Look, looking at, um, the pulled porks that we, that I’ve done for the US show in the last year, uh, we’ve got about a 60% success rate on them.

40% have gone down since I did the pulled pork. 60% have gone up,

Tony Kynaston: Mm-hmm.

Cameron: which is, you know.

Tony Kynaston: It’s

Cameron: The sort of run rate that we look for you,

Tony Kynaston: Warren’s

Cameron: you know,

Tony Kynaston: It’s my long-term average. Yeah.

Cameron: not all of them are gonna be winners and I dunno, the PCG will be, I dunno that this will be, but you know, we se we sell the ones that break our cell rules and we hold the ones that continue to [00:18:00] do well.

Uh, book value, uh, equity per share when I break it down into US dollars is about $25 11, and book plus 30 would be $32 64. Um, the current share price, as I said, is about $16 74.

Tony Kynaston: we can buy it for half a book. That’s

Cameron: 1.5 Price to price to operating cash flow and half book, uh, 0.67 times book. So deep value territory?

Tony Kynaston: So that I, I, it is wonder, I am wondering whether that means the assets need replacing.

Cameron: Yeah. Quite possibly. Yeah. It’s above, well, like our IV one is $4 33, our IV two is $5 eight, so it’s well above those. But, uh, looking at the rest of the [00:19:00] numbers, So it had a QAV score of 0.56, which is why it was at the top of the list. Average daily trade’s about 7.6 million. Pr/OpCaf we’ve talked about. Quality rank is 50 in stock Edia, so it doesn’t score for that. Stock rank is, uh, gets a score. It’s above 90. Uh, I don’t have, I’ll get to it later. F score, as I said, is an eight, so it scores for that.

Um, and, uh, what else? Uh, prices not less than IV one, not less than Iiv two does get the book, doesn’t have a new point. Upturn, um,

Tony Kynaston: What’s its

Cameron: book value growth isn’t positive, not great. Yield’s low. The yield is like, yeah, they’re not paying a huge dividend. I guess they’re. Investing it back into the business. I assume I do have some notes on the yield here.

Yield TTM is 0.43%, basically nothing.

Tony Kynaston: Wow.

Cameron: They have been more generous in the [00:20:00] past, but they’ve just come through these crisis years. So they slashed or suspended dividends to conserve cash and appease regulators who didn’t want them paying large dividends while households were angry about tariffs or something.

I guess. So that may come back in the future. We’ll see.

Tony Kynaston: Yeah. And by tariffs you mean prices? prices, not tariffs between countries.

Cameron: No. Yeah. Uh, you know, the regulated electricity prices that they have there. So all in all, uh, they actually would’ve got a 10 outta 13 once I accommodated for the. Um, difference between the one and the US dollar. They got an 11 when I did it, but I had to adjust it. It’s about an 80% quality score on our scoring and, uh, yeah, a really strong QAV score.

So, uh, that is, stock rank is [00:21:00] 95, by the way. Um, that is. Korean electric power and I have added them to our portfolio. So let’s see how they go.

Tony Kynaston: good.

And you know, as we spoke about in the Australian show, there’s mean these are kind of, um, these utilities, even though they might not compound, um, like a growth stock, they’re, you know, wait until there’s a downturn in the market. And nobody turns their light bulbs off, they still keep needing electricity and this stock will just keep chugging away.

So in the long term it is, you know, these businesses are stable and they throw off lots of cash, which can not in this case immediately ’cause they were, have regulatory problems, but eventually will lead to high dividends or buybacks. And so, um, people will benefit from that point of view.

Cameron: At the end of the day, I just look at it as a company that’s generating a ton of cash that you can buy for nothing. So it’s a lay down Mabb [00:22:00] air from my perspective. And

Tony Kynaston: Agreed.

Cameron: if it goes belly up, it goes, like if things go badly for it in the future, we sell it and buy something else like, but based on the numbers that it has today, it’s a no brainer.

Tony Kynaston: time, isn’t it? Good time to buy?

Cameron: Well for us, but I guarantee you when I post this to Reddit, everyone will be just be, you know, furiously angry at, uh, why it’s such a bad idea and why they should be buying Google. Somebody with the PCG one, somebody said, I think Google is overpriced, but I’d double down on Google before I’d buy this dog.

Like, yeah, go for it, son.

Tony Kynaston: makes

Cameron: Good luck with that.

Tony Kynaston: more.

Cameron: By the way, Google is like Google’s AI stuff that’s come out with this week is insane. Um, I’ll show you something in a minute. Um, off air before you go, before your furniture turns up. But, uh, yeah. Anyway, uh, that is QAV America for this week, Tony.

Tony Kynaston: [00:23:00] cam. That was good.

Bernard: Q A V is a checklist-based system of value investing developed by Tony Khighneston over 25 years. To learn more about how it works and how you can learn the system, visit our website, Q A V Podcast dot com.

This podcast is an information provider and in giving you product information we are not making any suggestion or recommendation about a particular product. The information has been prepared without taking into account your individual investment objectives, financial circumstances or needs. Before you decide whether or not to acquire a particular financial product you should assess whether it is appropriate for you in the light of your own personal circumstances, having regard to your own objectives, financial situation and needs. You may wish to obtain financial advice from a suitably qualified adviser before making any decision to acquire a financial product. Please note that all information [00:24:00] about performance returns is historical. Past performance should not be relied upon as an indicator of future performance; unit prices and the value of your investment may fall as well as rise. The results are general advice only and not personal product advice.

Transparency is important to us. We will always be very open and honest about the stocks we own. We will also always give our audience advance notice when we intend to buy or sell a stock that we are going to talk about on the podcast. This is so we can never be accused of pumping a stock to our own advantage. If we talk about a stock we currently own, we will make it known that we own it.

This email is authorised by Anthony Khighneston Authorised Representative Number zero zero 1 2 9 2 7 1 8 of M F & Co. Asset Management Proprietary Limited [00:25:00] (A F S L five 2 zero 4 4 2). No part of this content may be reproduced in any form without the prior consent of Spacecraft Publishing.

Here’s an update on the performance of the other stocks we’ve done as a pulled pork (deep dive) since the start of the show. Average return so far is 44%.

0 Comments