Episode Overview

This episode dives into Pacific Gas & Electric (NYSE: PCG) and its strange mix of monopoly power, criminal convictions, billions in liabilities, climate exposure, and a CEO who says she’s “leading with love.” Cameron takes us through PG&E’s century-old origins, deadly infrastructure failures like the Camp Fire manslaughter convictions, the bizarre history of repeat explosions and corruption, and the unusual financial structure that keeps the company alive despite $58B in debt. Tony questions whether a guaranteed utility should even be privately owned, compares it to safer options like Berkshire Hathaway’s utilities, and wonders why we’d touch a business known for burning down half a state. Despite the horrors, PG&E lands on the QAV buy list due to cheap cashflow valuation, a protected regulated monopoly, and a massive turnaround driven by mandated wildfire-prevention spending and government-backed debt.

Timestamps

00:00–02:00 US Portfolio performance update General markets

02:00–03:30 MODG rises after last week’s pick MODG (TopGolf Callaway)

03:30–04:30 Recent picks performance rundown

05:30–06:30 AU market outperforming “trash” theme Australian context

06:30–41:00 Feature Deep Dive: Pacific Gas & Electric PCG

41:00–47:00 After-hours: Stalker, House of Guinness, Slow Horses

Transcription

Cameron: Welcome back to QAV America. Tony, I would ask how you’re doing, but I know because we just did our Australian podcast and you’re doing great. Let me answer that question for you.

Tony Kynaston: I’m doing great. My portfolio is doing great. Everything’s great.

Cameron: Everything’s great. Our US portfolio, Tony, I’m just bringing it up on the screen here all time. So it’s been running since, uh, September, 2023 is up 55% versus the benchmark I use the s and p 500, which is up 50%.

So we’re doing 10% better than the benchmark, 55% over. A little more than two years. It’s not bad. Pretty happy with that.

Tony Kynaston: I agree.

Cameron: Pretty good.

Tony Kynaston: We normally say it’s up 5% though, so usually you take one away from the other rather than make a percentage of a percentage.

Cameron: [00:01:00] Okay.

Tony Kynaston: better, but

Cameron: But if we’re saying double market, then that’s a hundred percent. Isn’t that? How do you say that? If we’re saying double market.

Tony Kynaston: Well, double market’s just double market.

Cameron: It is double

Tony Kynaston: market. Yeah.

Cameron: twice as good. Okay. Um, some of the, uh.

Tony Kynaston: raise that with me and said, are we better off saying we do five to 10% better than the market? ’cause in Australia, I guess in the US as well, the long term’s, about 10%. So, um, I said, yes, if the market does 10%, it’s right. But if it’s doing, if it’s up as in the America, America, it’s, um, it’s wrong.

Cameron: Yeah. Right.

Tony Kynaston: Mm-hmm.

Cameron: Some of the, uh, just looking at the last, uh, let’s say the last 30 days in our portfolio, our portfolio is beating the index in the last 30 days. Uh, not by a huge amount, but by, well actually I guess judging by [00:02:00] the way you are rating it, s and p is up 0.13% in the last 30 days. Our portfolio is up 0.61%, so that’s five.

Five times better. That’s what I was gonna say. Yeah. Uh, the,

Tony Kynaston: I like the core skill of marketing. Okay. It’s great.

Cameron: yeah. Uh, unfortunately stocked doesn’t tell me how the individual stocks have performed in a 30 day period. It just gives me it from the get go. But, uh, I did want to just look at our, uh. Performance of some of the other stocks that we’ve, uh, talked about over the, uh, last six months or so. We’ve been doing the show, see how they’re all doing.

You’ll be happy to know that the company that we talked about last week, top Golf, Callaway Brands, [00:03:00] M-O-D-G-A-K-A, modern golfers up 3% since we talked about it.

Tony Kynaston: fantastic.

Cameron: Um, some of the others aren’t.

Tony Kynaston: little putt,

Cameron: Yeah, that was us. That was all our putt. Yeah, that was, that was all our putt. Yeah.

Tony Kynaston: another

Cameron: IS

Tony Kynaston: that I can get excited about? Do you have a

Cameron: uh, no, I’ve got some horrifying, horrible stories to talk about this week, but, uh, it should be fun.

I wanna admit, I saw a video the other day yesterday of a golf robot that got a hole in one. Have you seen that?

Tony Kynaston: No.

Cameron: I thought that’s the next evolution. I know for your 60th birthday, we got you a robot, uh, caddy.

Tony Kynaston: Catty.

Cameron: Uh, we’re gonna get you a golf robot for your 70th birthday. You don’t have to do anything now.

You just go out there, plays golf for you. It’ll be fantastic. You’ll love it. Uh, so American Airlines we talked about a couple of weeks ago, it’s down 10%. Um, American Axle is down 1%. Cal [00:04:00] Main Foods is down seven. Community health is stable. Methodex is down 10. Um, Titan Machinery is down 19. But outside of that, we’ve got quite a few winners.

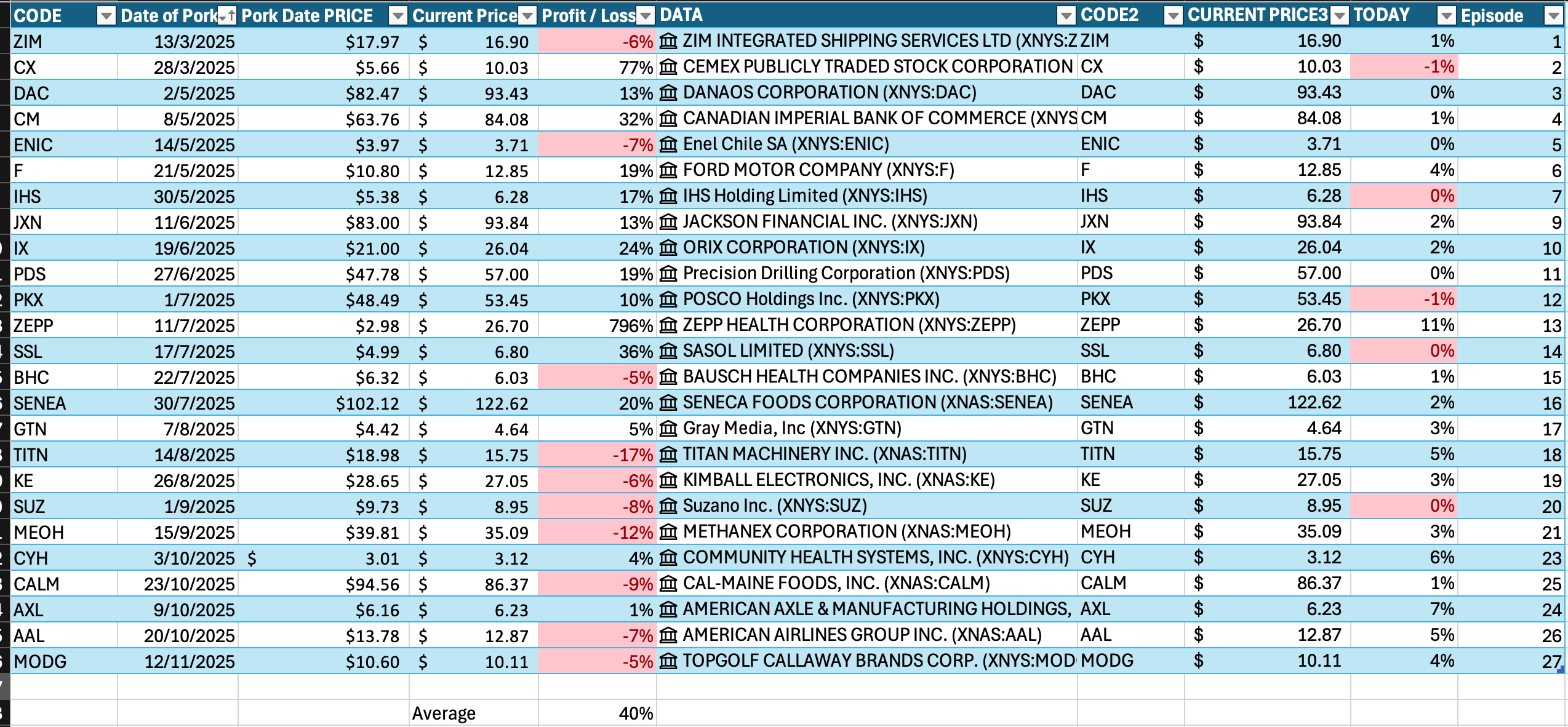

Uh, Chemex is up 77% Canadian. Imperial Bank is up 36. Zep Health Corporation, which somebody on Reddit said was a Chinese fake stock is up 705% since we talked about it. The average of all the companies that we’ve been covering in our deep dive segment since March, their average is a 37% return on them, uh, over the course of that period.

So they’re not all winners. There’s, there’s about 30% are actually down now, the rest of winners, but the US market. Interesting and challenging this year. It’s funny, we just did, in our Australian show, we talked about an analyst from Macquarie Bank saying all the companies that are doing well in Australia are the [00:05:00] trash.

It’s been a dash for trash, but our portfolio’s going great. Guns in Australia, and they’re all good value stocks generating a lot of cash.

Tony Kynaston: Yeah,

Cameron: the same sort of stocks that we’ve had in the US not doing as well in the us um, because the market over there, well, not as well as they’re doing here. Yeah. Okay.

Yeah. But the Australian portfolio is up about, what’d I say? It’s up 40, 37% this year or something.

Tony Kynaston: I think you said? Yeah.

Cameron: Oh yeah, no, that was in the last six months. 26% In the last six months. It’s up like 37% this calendar year. It’s crazy. But the company that I’m gonna talk about today, Tony is Pacific Gas and Electric Company.

Did you watch the Electric Company in the seventies?

Tony Kynaston: Yeah,

Cameron: That was a great show, wasn’t it?

Tony Kynaston: first went to.

Cameron: Before it was like Sesame Street. We’d on here in Australia, we’d have Sesame Street and sometimes the electric company would be on [00:06:00] instead of it or after it. Um, I dunno what happened to that show, but I remember loving it as a kid.

Dunno anything about it though. I don’t. Was it a Henson show? Don’t even know.

Tony Kynaston: a Henson show. Yeah,

Cameron: Was it? It was.

Tony Kynaston: I think so. Yeah.

Cameron: But this is not that, that, uh, electric company, this is, uh, their ticker code is PCG. They’re, they go by pg and e and, uh, wow. What a story. What a story.

Tony Kynaston: Electricity is brought to you by the letters P, g and

Cameron: C and g. Yeah. Oh man. This is, uh, one of the oldest and largest utility companies in the United States. They supply electricity and natural gas to roughly 5.2 million households or 16 million people across northern and central California. Their job is basically to keep the lights on and the gas flowing.

They operate one of the,

Tony Kynaston: can I interrupt there?

Cameron: yeah.

Tony Kynaston: So it’s one of the largest gas and electric companies that [00:07:00] supplies how many people? 16 million.

Cameron: Yeah, that’s it.

Tony Kynaston: That’s it. Are there a lot of fragmented utilities in America? Are there

Cameron: I guess there must be, and there one, there’s like five or six big ones just in California alone, but the, the area that they cover is quite large and quite complex. It’s like northern and central California. So I don’t think it’s like, it’s not, uh, la it’s like sort of more regional parts of California. Um, they operate one of the most complex and climate exposed power grids in the world.

70,000 square miles of mountains, forests, farmland, and dense urban centers. But what makes them most unusual is they are the only major American power company. That has been criminally convicted of manslaughter, forced [00:08:00] through multiple bankruptcies and publicly blamed for catastrophic wildfires and wow.

And that’s just the tip of the iceberg, the scandals that they have been through over the years. It’s, uh, man, you could make a whole Netflix series over these guys. Uh, and I’ll tell you about a couple of them just for the salacious fun of it. In 2018 and 2019 investigations by the California Department of Forestry and Fire Protection, AKA Cal Fire found the company’s infrastructure primarily responsible for causing two separate devastating wildfires in California, including the 2018 campfire.

The deadliest wildfire in California history caused 85 fatalities, displaced more than 50,000 people destroyed more than. 18,000 structures and caused an estimated 16 [00:09:00] and a half billion dollars in damage. And because California holds utilities financially responsible for any fires caused by their equipment, even if maintenance was properly done, there was a $30 billion liability.

That the company was facing and they declared Chapter 11 bankruptcy in 2019. They made a settlement offer of 13 and a half billion to the wildfire victims, and, uh, they pled guilty to 84 counts of involuntary manslaughter.

Tony Kynaston: You were saying before about the US at the heart of the US as lawyers and at the heart of China as engineers,

Cameron: Hmm. In China, they would’ve just shrugged and said, get back to it.

Tony Kynaston: not

Cameron: Build more. No, it’s just build more electricity grid. You gotta break a few [00:10:00] eggs. Um. The campfire was caused by the failure of a single metal hook attached to a pg and e transmission tower on the company’s Caribou Palermo transition line transmission line, which carried power from hydroelectric facilities in the Sierra Nevada to the Bay Area Towers a little under a hundred feet.

30 meters tall was built on a steep incline on a ridge above Highway 70 in the North folk, north Fork, sorry, feather River near the community of Ger. The. Tower had two arms each, each with a hook hanging from a hole in a long piece of metal. The hook held up a string of electrical insulators. The transmission power lines were suspended from these insulators away from the steel tower itself, so as to prevent electricity arcing between them.

One of the hooks on the tower about three inches and one inch in diameter. [00:11:00] Had been worn down by rubbing against the metal plate that it hung from, to the point where only a few millimeters of metal remained. Dunno why Wikipedia, where I’m getting this from is switching between inches and millimeters.

That’s confusing for Americans, but yeah, however many tens of an inch that is. Um. At 6:15 AM on November 8th, the pg e control center in Vacaville recorded an outage on the company’s transmission line in the Feather River Canyon. The hook had snapped. Under the weight of the power line, an insulator string that it supported, which weighed more than 142 pounds, 64 kilos, no longer held up.

The energized power line struck the transmission tower. This created an electric arc between the power line and the tower, which reached temperatures estimated at 5,000 to 10,000 degrees Fahrenheit, which is for the rest of the world. [00:12:00] 2,800 to 5,500 degrees Celsius and melted metal components of the conductor in the tower.

The molten metal fell into the brush beneath the tower setting at a light. The fire burned for two weeks and was contained Sunday, November 25th after burning 153,336 acres.

Tony Kynaston: Well, I guess you’ve gotta question design of that whole system. If it’s, you know, if it’s from catastrophic failure by a three inch hook, you, you know, might have worked for a long time, but it’s got a weak point, hasn’t it really as

Cameron: job needs to be to go check the hooks. Yeah.

Tony Kynaston: Well just, well come up with a different solution.

Cameron: Well they have, and I’m happy that you suggested that. I’ll talk about it. Um, all good though. The CEO at the time was a lady by the name of Geisha Williams. She left and [00:13:00] was replaced eventually by another woman, and I’ll talk about her a little bit, little, a little bit later on. But I watched an interview with her where she said she is leading with love.

That’s her whole philosophy is leading with love. So that’s good. I like that tr try to kill less people. We’re leading with love. We’ve decided that business model. Yeah, we’re changing things. I’m turning it around. Um.

Tony Kynaston: called LWL, electricity

Cameron: Leading with love. Yeah, that’s nice. Look, you and I are all for women running things.

Your wife is a former corporate CEO, senior executive. We’re all about more women in positions of power.

Tony Kynaston: Absolutely.

Cameron: Hopefully they don’t kill 18,000 people. But you know, same thing probably would’ve happened if a guy was running it. Uh, pg e’s founding [00:14:00] goes back to 1905 when a group of California hydroelectric pioneers merged their operations.

They were classic west coast industrialists mining engineers, early power entrepreneurs, dam builders who wanted to electrify San Francisco and the surrounding valleys. Think Chinatown, Jack Nicholson, but instead of orange. Groves, it’s, there was a lot of actually water in that too, wasn’t there? There was like

Tony Kynaston: water.

Cameron: redistributing the water and, yeah, that’s right.

Mm-hmm. Mm-hmm.

Tony Kynaston: No. Was it making water? Getting water to the orange farmers or getting it away from it? I can’t remember. Yeah.

Cameron: Yeah. Yeah, I think it was property development. They were trying to get it into the areas where they were gonna r

Tony Kynaston: You are right. Yeah.

Cameron: the land to build big residential areas. The company grew as the gold rush towns and farming belts boomed, [00:15:00] stringing wires across vast distances where no one else bothered. Then it grew into a regulated monopoly.

Built nuclear plants survived a major corruption scandal in the 1990s involving illegal back channel lobbying, which I’ll talk about a little bit later on. Uh, the 2010 San Bruno Gas Pipeline explosion killed eight people triggering criminal cases and hundreds of millions of dollars in fines. Um, they have had a story to tell.

I, I’ve,

Tony Kynaston: I’m

Cameron: I think I’ve got,

Tony Kynaston: after this cam. I feel very uncomfortable talking about this misfortune of people.

Cameron: yes. It’s terrible. And, you know, I’ve done a lot of pulled porks on these American companies with really. Dirty, murky, horrible backstories, but they’re turning up on our buy list partially because of these things. I think they’re like PR nightmares and potentially lots of potential future exposure to more of these sorts of issues as well.

I, [00:16:00] I think they’re discounted the CEOs. This, as I said, uh, the current CEO is a woman called Patty Poppy, which is a great name. Poppy is the first.

Tony Kynaston: Patty Poppy, leading with love.

Cameron: Poppy.

Tony Kynaston: That sounds like

Cameron: Uh,

Tony Kynaston: Christian albums from the sixties.

Cameron: well, I was gonna say she sounds like, uh,

Tony Kynaston: she plays the

Cameron: um. Like an r and b singer from the sixties, you know, Patty Poppy, and, uh, with a, you know, my baby loves me, sort of, uh, you know, r and b hit Poppy is the first female executive to serve as the CEO of one Fortune 500 company and then become the CEO of another Fortune 500 company.

She was formerly the president and CEO of CMS Energy. From 2016 to 2020, and then she left to become pg ECEO in 2021. And as I said, she talks about leading with love. And, um, yeah, I, I watched this interview with her. It was very interesting. [00:17:00] Uh, the new chief commercial officer just announced this week is also a woman.

Uh, shell, Izzy is the, um, chief Commercial Officer. She’s a clean energy pioneer. She ran a clean energy. Startup and a few other things before this. But she said, uh, well, the company said in her announcement that her job is basically to work with all of the AI data centers in that part of California that are trying to suck up all of the energy and figure out how to supply them without everyone else having to suffer and paying higher prices, et cetera, et cetera.

But the campfire from 2018 is just one of the horrors this company’s been through. Um, uh, in. On April 16th, 2013, a team of gunmen opened fire on the Metcalf Transmission substation in Coyote, California. The attack damaged 17 high voltage transformers caused more than $15 million in damage. They also cut fiber optic [00:18:00] telecommunications cable, owned by at and t, pg and e, and at and t offered a $250,000 reward for anyone who had information leading to the arrest of the culprits.

But they were never found. It was like some sort of an attack on their infrastructure and.

Tony Kynaston: Mayhem?

Cameron: Yes. That’s what it sounds like, right? Yeah. Project Mayhem. Uh, his name was, what was his name? His name was, no, no, no. When, when, um, meatloaf gets killed in it. Yeah. They’re like, he had a name. His name was something, I can’t remember what his name was.

Um, the, the explosion I mentioned, um, briefly before in 2010 in San Bruno, um, a suburb of San Francisco was damaged when one of their natural gas pipelines that was at least 54 years old, 30 inches in [00:19:00] diameter, located under a street intersection in a residential area exploded. Sending a 28 foot section of pipe

Tony Kynaston: Oh.

Cameron: weighing 3000 pounds.

Flying through the air, the. This is before the love. They weren’t leading with love. They were leading with explosions. Back then, Tony, uh, the blast created a crater at the epicenter and killed eight people, injured nearly five dozen more while destroying about a hundred homes. In 2016, they had the ghost ship Warehouse fire in Fruit Vale Oakland, California.

Fire broke out in a former warehouse that had been illegally converted into an artist collective with living spaces known as Ghost Ship. 80 to a hundred people were at an event in the space and 36 were killed. The plaintiffs claim that the fire was caused by an electrical malfunction. in [00:20:00] 2020, pg e settled a civil lawsuit for 32 of the victims out of the 36 who perished in the fire.

I could go on lots and lots of juicy, juicy scandals over the years. I mean, it’s like, it’s just one of these businesses. There’s, in Wikipedia, it’s just got page after page after page of horrible, horrible stories. Anyway. Where it is today is has its electricity operations, which is about three quarters of the revenue and the gas operations, which is the rest, and.

They’re doing a lot actually to work on avoiding more disasters. They’re pouring enormous amounts of money and they have an enormous amount of debt, but they’re pouring enormous amounts of money into grid hardening. They’re burying thousands of kilometers of power lines expanding automated fire risk monitoring systems, [00:21:00] shifting parts of the network to microgrids and remote shutoffs.

So they’re doing a lot of work to try and, you know, de-risk the business, I guess, which is interesting. But, uh, you know, it’s costing tens of billions of dollars to do this. But I guess when you get, have to go into bankruptcy because you owe $30 billion in, uh, damages, uh, then investing to prevent more of those from happening.

And of course, as we know, uh. Despite what the Trump administration will tell you, climate climate’s getting hotter, California’s gonna be getting hotter. The the risks for of fires I imagine are increasing in California and uh, it’s gonna be more expensive to ensure things your liability risk is gonna go up.

Um, so I’m sure Gavin Newsom and the Californian government, uh. Gonna [00:22:00] make it harder and harder for these companies to, uh, you know, uh, uh, uh, get away with this sort of stuff. Make sure that they’re cracking down on them even further. But they, they’re an interesting business because they have a regulated rate base, uh, uh, uh, unlike Australia, well, at least I don’t think it works that way here.

Uh. In the us if you build infrastructure that gets approved by the regulators, you get a guaranteed return on that asset. You’re ex power company. Do we have regulated, well, I know it was Shell, but do you do, do we have, do we have regulated guaranteed returns for

Tony Kynaston: No,

Cameron: in Australia?

Tony Kynaston: no, they, they do

Cameron: It’s,

Tony Kynaston: to approve price increases and the like, but no, there’s no guaranteed return

Cameron: well, you know, as.

Tony Kynaston: of anyway.

Cameron: America’s a much more socialist country than Australia, Tony, when it comes to these things.

Tony Kynaston: Yeah.

Cameron: No, this is in the us. I [00:23:00] don’t think this is just California. I think this is across the us. Um, so the bigger the rate base, the bigger the allowed profit pool. This is how all US utilities, US utilities work as far as I’m aware, but their rate base is exploding because of mandated wildfire hardening projects.

They’re undertaking massive CapEx to convert all of these lines and push them underground. And a, a case study I came across said that putting them all underground could reduce wildfire ignition risk by up to 98% compared with overhead lines. So it’s a, it’s a big deal.

Tony Kynaston: Yep. Still not a hundred though, is it?

Cameron: It’s what?

Tony Kynaston: It’s still

Cameron: Not a hundred? No, it’s still not a hundred percent, no. Yeah. Um, they’re also spending a fortune on improving weather monitoring analytics systems and integrating weather models into operations. So they’re, I think when things are gonna get hot, they’re [00:24:00] turning power off in certain areas to further reduce the risk and.

Upsetting people, but they’re like, oh, we gotta turn the grid off here. Or downscale the amount of power that’s a available, but there’s this thing called the California Wildfire Insurance Fund. The CWF that was established in 2019 to cover certain utility caused wildfires participating, investor owned utilities, which include.

PG e contribute capital and are eligible for loss reimbursement when a covered wildfire is determined. The fund currently has a design capacity of $21 billion and has been expanded for future years while the wildfire continuation account, so it’s sort of a, a, a. A cushion for pg and e and the other utilities.

If there’s a utility ignited fire that causes large losses. They have their own insurance fund, I guess, so it’s.

Tony Kynaston: the, the energy companies or contributed by the government [00:25:00] the, the rate post.

Cameron: No, as far as I’m aware, it’s the investor owned utilities that contributed capital to it, so they created their own fund, but they do get, they are getting cheap loans from the government to do a lot of the work that they’re doing as well. Which I’ll get into when I get into the debt story in a section in a, in a second.

But the interesting thing about them as a business, as I said before, is they kind of have, um, a moat, I guess, on this footprint. No one, no one can compete in this footprint that they’ve got. They, it’s their man. Well, yeah, that’s a good question. Yeah. But their monopoly is legally protected

Tony Kynaston: Right.

Cameron: now. I, I don’t know about how solar power plays into that.

Like if I don’t know what the solar power penetration is in California, I, I know in Australia it’s insanely high now. I read an article a week or so ago, [00:26:00] I think in the financial review here, saying that there was one point last week or last month when. Uh, solar power and wind contributed more energy into the Australian grid than traditional, uh, sources of energy did.

Tony Kynaston: Yeah. Which causes all kinds of problems, of course, because you know, you’re trying to make a, make a base load. Power station still work and. guess work profitably and then it’s being flooded by solar.

Cameron: Yeah.

Tony Kynaston: by solar. Yeah. It’s hard.

Cameron: Yeah. Yeah. Hard for the businesses. Yeah. And the people running the grids.

Tony Kynaston: Well, I was gonna say people running the grids too, just trying to balance everything out. ’cause you,

Cameron: Yeah.

Tony Kynaston: like, you can’t just flick a switch in a, in a power station and shut off the turbines. They, they get taken out over a long periods of time and then if they’re needed, quickly,

Cameron: Yeah,

Tony Kynaston: of time to get them back up to, to speed again.

Cameron: yeah. So, um. [00:27:00] Yeah, so it’s legally protected. So they’ve got a, they’ve got a moat there, but, and they’ve also got, uh, uh, I mean, they’ve got a political moat as well. The state needs pg and e. They need them alive. They, they need to be providing power to this part of California. Someone has to run a system across all of these fire prone regions, but it also comes with risks, but they’re trying to de-risk it, as I said.

Uh, it, it is quite cheap, and I’ll go through the numbers shortly. How much time have we got? A few more minutes. The boring reality is they’ve had a lot of, uh, really tragic instances, but they’re slowly de-risking themselves. But the market doesn’t really seem to be factoring that in, you know, they’re, the market’s more, I think risk prone when it comes to looking at pg e, they’re sort of mid turnaround.

As I said, they’ve got a ton of ton of debt, but, uh, if they could pull this off, they can keep their cash flows [00:28:00] up and stop having. Major disasters that they have to pay for. Then long term, it could be a, a healthier business, let’s say, than it has been in the last 10 years. Although there’s also EV adoption too, which is another thing that, um, my notes pulled up as well.

California’s pushing for grid expansion to support EV adoption and renewable energy mandates, which also plays into their business model quite well, you know. So they carry a huge pile of debt. Um, I’ll just open their, uh, page on stock Edia again, so I can have those numbers in front of me.

Tony Kynaston: Keep giving Proctor and Gamble when I’d go on encyclopedia and put in pg

Cameron: Ah,

Tony Kynaston: PCG.

Cameron: right. Uh, net total revenue [00:29:00] TDM is 24.7 billion. Operating profit TTM is four and a half billion net profit, 2.7 billion, net debt, 58.9 billion.

Tony Kynaston: Oh,

Cameron: Yeah, net fixed assets, 123.8 billion. Book value, 30.4 billion, but it’s a ton of debt. Big, big debt. But as I said it, it comes from a variety of, uh, sources and it’s structured in quite an interesting way.

It’s not normal corporate leverage. Like you look at that on the surface and you go, well, $59 billion worth of debt. That’s insane. But it’s a Frankenstein mix of high risk bonds and state engineered cheap loans

Tony Kynaston: Right.

Cameron: designed to keep the utility alive.

Tony Kynaston: Mm-hmm.

Cameron: They’ve got some traditional corporate debt, which still attracts.

High interest rates because investors remember the bankruptcies and [00:30:00] what a factor in another potential billion dollar wildfire. But the cheap stuff sits in what are called recovery bonds that California allows them to issue. They’re not repaid by pg and e, but by automatic surcharges on customer bills.

Tony Kynaston: The customer pays,

Cameron: The customer pays Tony,

Tony Kynaston: so, so it’s a tariff.

Cameron: I guess. Yeah, and you know, we know tariffs don’t put up prices. Uh, Donald Trump has assured us of that, so it’s all good.

Tony Kynaston: way to do it.

Cameron: It’s all good. I guess they’re saying, listen, you want electricity, so you, someone’s gotta pay for us to, you know, run, keep running the business. You want the electricity, you’re not getting it from anywhere else.

We’ve got a, we’ve got a mandated guarantee.

Tony Kynaston: government just go and

Cameron: I,

Tony Kynaston: PG out of, uh, when it filed for chapter five for chapter 11? And [00:31:00] then there’s no profit margin and rate pays are

Cameron: well. I keep telling you that the Australian government should just buy all of our mining companies and aren’t paying any tax. You tell me we can’t do that.

Tony Kynaston: we can do that. Can do it if we like. I think a better solution in terms of the Australian Mining industries is to charge them 1% royalty and what they dig out of the ground and then put that into a future fund. Um,

Cameron: do that? Isn’t that how we funded the Future Fund?

Tony Kynaston: no, the Future Fund was funded by the sale of Telstra.

Cameron: Oh yeah, that’s right. Yeah.

Tony Kynaston: And in fact, I think that Telstra was sold off after it was found liable for the Black Friday bush fires. Uh, and had to spend a lot of money going through and fireproofing its network. Similar sort of story. They, um,

Cameron: Really

Tony Kynaston: dunno if, if you drive through a street, certainly down in Victoria where the bush fires happened, you’ll see all the trees are half cut off. ’cause they have to keep a certain distance away from the,

Cameron: right.

Tony Kynaston: power lights.

Yeah.

Cameron: Power [00:32:00] lines. I think Kevin Rudd, our prime minister in the 2000, late two thousands tried to use a mining tax to fund something and

Tony Kynaston: well, he, well,

Cameron: he.

Tony Kynaston: she took over when? Yeah. During her whole kerfuffle. Yeah.

Cameron: Yeah, I think he tried to do it, then he got kicked out, then she did it and she got kicked out and he came back and then he got kicked out. And yeah,

Tony Kynaston: Yeah.

Cameron: any who back to pg and e. So they look wildly leveraged on paper, but, uh, a fairly large slice of that is low risk, low interest, almost like a municipal debt.

Um. It’s sort of, there’s some sort of state mandated true ups to guarantee repayment, sort of, it’s basically backed by the state rather than the company, which softens some of the financial risk, even though their operational and political risks, you know, remain high until this whole de-risk of re deification, I guess has happened.

Um, quickly just running [00:33:00] through the numbers. Um. Uh, some of the key ones for us is the price to operating cash flow is 4.21, so four years roughly to get back your investment. It’s, uh, you know, relatively short timeframe, but, uh, that is probably the only really good number I have for them. I’ll, I’ll go through all of the numbers, um, so you can see where it stands.

Let me open this window up a bit more. It doesn’t score great on our system, but it scores well enough to be on our buy list. The QAV score is 0.12, so it’s fairly low down on our buy list. But again, I picked it this week just because it was a terrific story. I actually, I actually have a, you know, there’s a hundred plus stocks on our buy list every week in the US buy list, and I, what I do now is I just give them all to ChatGPT.

I say, pick me. Pick me one of these. That’s gonna be a [00:34:00] good, that’s got a good story to tell and let it do the work. ’cause I used to have to go through them one at a time. ’cause I dunno, most of these companies and it’s like, oh, shipping company, shipping company, shipping company, financial services company, shipping company, financial.

And no, I was just give it to GPT and I said, oh yeah, you want a good story, pick this one. And it was not wrong, I gotta say, um,

Tony Kynaston: I have to

Cameron: so.

Tony Kynaston: Australian show.

Cameron: Yeah, just pick one for me. Average daily trade is $400 million. Um, now the, the stocked numbers not great quality rank is a 21. We only give it a score if it’s 60 or above, so it didn’t score for that.

Stock rank is a 36. We only score for a 90 or above. F score is a four. We only score for 4.5, so it’s sort of little bit less than that. Middle of the road, uh, doesn’t score for our IV number one, our IV number one, our intrinsic value. Number one is a six point is $6 90, sorry. And the share price when I did it was [00:35:00] $16 49.

Our intrinsic value. Number two, our future looking intrinsic value is 14.8, so it’s below that. Uh, sorry, it’s above that as well. $16 49. The share price, the book. Price is, uh, $13 70. So the share price is above that and we can’t score for it. But book plus 30 is $17 80, so it did score for book plus 30. Um, it’s got a positive uptrend, but not a new upturn.

Um, PE is, um, not less than the yield. Yield is. Not greater than the bank debt. Forecast of IV is not greater than twice the share price. So it got a quality score, a, a QAV quality score of only 50%. And as I said, the QAV score is quite low, 0.12. So look, not the best, most compelling stock that I’ve seen on our buy list, but it does [00:36:00] have, as I said, it’s basically got a guaranteed income stream.

Which is unusual and it’s quite cheap in terms of, you know, the price to cash flow anyway. And even the price to book is, it’s, it’s above book. Price is above book, but not by much. It’s like 20% above book, which is relatively reasonable for a company with guaranteed income, guaranteed cash flow anyway. Um,

Tony Kynaston: We

Cameron: and some,

Tony Kynaston: proxy in Australia for, for those kinds of businesses. So it’s. Got of a guaranteed cash flow, paying, throwing off a, you know, certain dividend coupon.

Cameron: With huge risks, but then it’s got this, this fund that’s gonna ameliorate some of that. Obviously the state needs it to exist. It’s gone through bankruptcy. Once

Tony Kynaston: So the fund’s interesting,

Cameron: I.

Tony Kynaston: Like you’re spending tens of billions dollars to fireproof your. Network, but you’re also putting into a [00:37:00] fund 10 tens of billion dollars of insurance premium. It’s like, which one’s? Right? It’s like, am I gonna fireproof the network, in which case I don’t need insurance, or I not gonna do as a proper job on the fireproofing and therefore I need insurance?

I guess a, an interesting paradox.

Cameron: Yeah, but I think the, the, the thing that’s got going for it the most, Tony, is it’s being led with love and, uh, that’s where the premium we, should we have a score for that in Q’S checklist moving forward? Is it led with love? What’s the love score, Tony?

Tony Kynaston: Yeah.

Cameron: Yeah.

Tony Kynaston: Put it in the checklist. You’re right. One point leading with Love Point one of a

Cameron: Oh, more than no, more than that. Um, the share price in

Tony Kynaston: chu, we give him a a point for

Cameron: chutzpah. Yeah.

Tony Kynaston: with love.

Cameron: To give you some perspective, uh, the share price, uh, in September, 2017 was $70 and it’s now 16. Yeah, so I can [00:38:00] understand. I mean, at 20, uh, uh, in January, 2019, it, it had fallen down to $7 from September, 2017 at 70 January, 2019 at seven. So it didn’t stay down there too long.

It recovered up to 23 by April. But, um, yeah, so I like shareholders have been burnt badly by this over the last.

Tony Kynaston: Chapter Elevens because they’re unsecured. Unsecured, you know, in the business, people with debt in the business probably have it secured somehow, or at least rate is a higher. Priority in the repayment. So they get something in the dollar, but shareholders don’t

Cameron: So what do you think after all that, Tony?

Tony Kynaston: I’m glad it’s down the, at the bottom of the buy list side, I wouldn’t have to buy it. I think

Cameron: Well, you know, I’m always.

Tony Kynaston: numbers stack up on the, on the

Cameron: The numbers stack up.

Tony Kynaston: They don’t stack

Cameron: Yeah.

Tony Kynaston: side. Saw it.

Cameron: No

Tony Kynaston: Hmm.

Cameron: they don’t. Yeah. But this is what our buy [00:39:00] list has given us. Uh, one of the things anyway.

Tony Kynaston: help and I can’t help comparing it to Berkshire Hathaway, which large investments in electricity companies, energy companies, um, in the Midwest. I think from memory, and I don’t recall them ever burning down half a state and killing people. So, um, yeah, maybe that’s prior management and current

Cameron: Warren,

Tony Kynaston: pedigree.

Cameron: Warren and Charlie led with love. Tony.

Tony Kynaston: They were good marketers. I’ll give you that. I never said they’d lead with love. They did say write your own obituary and then live up to it.

Cameron: Yeah,

Tony Kynaston: And I’m sure it

Cameron: well.

Tony Kynaston: killing 18,000 people ’cause of a malfunctioning in a hook in a $3 hook.

Cameron: Yeah, well, I think the hook was probably worth more than that, but yeah, it was a big hook. Very big hook, heavy hook. All right. Thank you, tk. Uh, that is

Tony Kynaston: story again.

Cameron: crazy story, right?

After hours, [00:40:00] man, I finished stalker. You know, I think I told you about stalker.

Tony Kynaston: It’s on my list. Yep.

Cameron: We finally finished. It took us like three weeks to finish it. Probably one of the greatest films I’ve ever seen.

Got no idea what it’s about. Got no idea what happens in it.

Tony Kynaston: Mm-hmm.

Cameron: Amazing. Highly recommended, and it’s got the greatest craziest story. After we finished it, I thought, it’s one of those things I’m like, okay, I need to know everything about this now, because it, because the every shot you could print and make a photo and put it up on the wall, like every shot is just beautiful atmospheric.

But I found out this director Tchaikovsky shot, the whole film spent like a year shooting it in this part of Estonia, um, where there was like, there were shooting in old [00:41:00] abandoned power factories and stuff that were all falling down and there was toxic chemicals and radiation and stuff. Anyway, uh, when they sent the film to a film lab and got it back, it was all unusable after shooting for a year.

Tony Kynaston: Because of the radiation exposure.

Cameron: No, because it was a new film stock. It was this Kodak film stock that was popular in the late seventies, blade Runner, star Wars films. Like that was shot on it, but it was dodgy. So they got a dodgy batch of this Kodak film stock, and then the labs in the Soviet Union didn’t know how to process it properly, so it was too dark and too green or something.

So he went back to the producers and they decided to do it again, and he fired his camera operator or the, the second producer or something like that. They went and they, and he fired the, his wife, who was the lead actress in it and replaced her with someone else. They went back and they shot it again? No, [00:42:00] the, the DP didn’t like his wife or something.

Tony Kynaston: and don’t buy that film anymore.

Cameron: Yeah. So they went back, they shot it again. This time he didn’t like it, didn’t like the, the performances in it. So he went back and did it a third time. Shot the movie three times

Tony Kynaston: wow.

Cameron: and then everybody died because of the toxicity and the radiation poisoning. He died, his wife died. The lead, one of the, one of the stars and there’s only three actors in it, uh, or three main actors died.

Um, one of the bunch of the crew got sick and died. Because of the toxicity and the radiation and everything that they were around in these things. Like it’s incredibly crazy. He was like 52 Kosky when he died. I always wondered why he only made like a handful of films is ’cause he died after making this film.

Tony Kynaston: Wow.

Cameron: Anyway. Highly recommend it. It’s crazy story, an amazing film [00:43:00] like, but it’s like a Lynch film. Just go, go along for the ride. You know? It’s a big, deep philosophical thing on faith and modern modernity and blah, blah, blah, blah, blah. Apparently I watched like three or four YouTube explanations of it afterwards and no one could explain it.

Everyone’s like, well, apparently he said something, but he was one of these guys like Lynch, who was like, no, every, everyone asked him to explain. He goes, no, get your own ex meaning out of it. Right? Just watch it shut up, you know? Anyway, so that’s good. What you got.

Tony Kynaston: I will. look it up. Well, we’ve, Jenny actually, first of all, Roddy and I watched the House of Guinness on Netflix. I dunno if you’ve seen that yet. And

Cameron: The beer,

Tony Kynaston: it. And

Cameron: the beer company.

Tony Kynaston: yeah, yeah, it’s a

Cameron: Oh, okay.

Tony Kynaston: I think it’s

Cameron: Oh,

Tony Kynaston: the people who made picky blinders. So it’s in that kind of style.

Cameron: right,

Tony Kynaston: kinda like succession from the 18 hundreds.

Cameron: right. Sponsored by Guinness. They produce it.

Tony Kynaston: invo involvement they have, but they, they must be involved somewhere.

Cameron: [00:44:00] Right.

Tony Kynaston: yeah, it’s really good fun, enjoyed it. uh, and then I watched it with Ruddy when he was down here and Jenny was away and then she came back and I said, you gotta watch this.

And we watched it again, with her. So yeah, thoroughly recommend it. Great soundtrack to it. Lots of Irish punk bands in the soundtrack. It’s got that kind of, um,

Cameron: 18 hundreds. Punk.

Tony Kynaston: guy Richie, feel to it. Uh,

Cameron: Right.

Tony Kynaston: yeah, modern music and period pieces. Yeah. So that was fun. Uh, we’ve named a horse, Charlie 99, Steve Mabb and I and Ya au, who’s been on the show years ago.

Cameron: Oh yeah.

Tony Kynaston: I own a horse, race Horse and we finally got Charlie 99 accepted as a name. So

Cameron: Nice.

Tony Kynaston: fingers, crossed. It actually does well, so we can, it’s always a risk when you name a race horse after someone that it

Cameron: Yeah,

Tony Kynaston: just runs badly. But anyway, hopefully

Cameron: yeah.

Tony Kynaston: So that was good fun. Uh, speaking of horses like forest runs tomorrow at Caulfield on Wednesday if anyone gets us some time. [00:45:00] And then lastly, it’s the climb a GM in Sydney on Friday. So if anyone hears this and they’re around at lunchtime, um, I’ll be in the climb head offices at

Cameron: Oh, you’re going up for it?

Tony Kynaston: Oh

Cameron: Wow.

Tony Kynaston: I’m. Standing for elect. I’m officially being elected director, so, um, I was appointed

Cameron: wow.

Tony Kynaston: the next Ag GM and now I’m facing an

Cameron: Ah, can I come down and ask you some hard questions, Steve? Main type questions.

Tony Kynaston: Or you can save it up till next Tuesday when you ask me questions anyway.

Cameron: Can I invite my old girlfriend along?

Tony Kynaston: Oh, no, I wouldn’t do that. It’s probably not, not safe for her, I don’t think.

Cameron: No, I can get her to feed me the questions so she can have a little, I’ll have a little earpiece in. She can, yeah. Um, well have fun with that.

Tony Kynaston: thank you.

Cameron: Uh, um, are you watching Pluribus?

Tony Kynaston: No. Is there any good?

Cameron: Fantastic.

Tony Kynaston: really?

Cameron: Really? God, yeah. Were you, you a breaking bad bed call Soul fan? I can’t, I can’t [00:46:00] remember.

Tony Kynaston: gotten halfway through them.

Cameron: Uh, okay.

Tony Kynaston: I,

Cameron: Well maybe not for you then.

Tony Kynaston: I like

Cameron: No.

Tony Kynaston: they do anyway, I, I go hot and cold on better. Cool. Salt.

Cameron: Right. You may not like it then. Um, and the chair company and the studio, and now we’re watching Slow Horses. I got Chrissy to sit down and watch the first episode with me. I’d seen the first episode or two, but got her into it because, uh, I was talking to our Kung Fu Sifu the other day and she said, uh, I said, what are you watching?

And she goes, oh, we just finished the last season of Slow Horses. We love slow horses so much. And so Chrissy goes, well, it’s good enough for the seafood then. It’s good enough for me. I

Tony Kynaston: We’ve been watching Down Cemetery Road, which is by the same author,

Cameron: The new one? Yeah.

Tony Kynaston: That’s

Cameron: With uh, Emma Thompson

Tony Kynaston: Who’s fantastic.

Cameron: and Rachel Griffiths. Not Rachel Griffith, who’s the other actress? Um, Rachel something.

Tony Kynaston: Yeah. Dunno.

Cameron: I know her from. A few other things she’s been in. Yeah. Yeah. that is QAV [00:47:00] America for this week. Have a good one.

Tony Kynaston: All right, bye.

Bernard: Q A V is a checklist-based system of value investing developed by Tony Khighneston over 25 years. To learn more about how it works and how you can learn the system, visit our website, Q A V Podcast dot com.

This podcast is an information provider and in giving you product information we are not making any suggestion or recommendation about a particular product. The information has been prepared without taking into account your individual investment objectives, financial circumstances or needs. Before you decide whether or not to acquire a particular financial product you should assess whether it is appropriate for you in the light of your own personal circumstances, having regard to your own objectives, financial situation and needs. You may wish to obtain financial advice from a suitably qualified adviser before making any decision to acquire a financial product. Please note that [00:48:00] all information about performance returns is historical. Past performance should not be relied upon as an indicator of future performance; unit prices and the value of your investment may fall as well as rise. The results are general advice only and not personal product advice.

Transparency is important to us. We will always be very open and honest about the stocks we own. We will also always give our audience advance notice when we intend to buy or sell a stock that we are going to talk about on the podcast. This is so we can never be accused of pumping a stock to our own advantage. If we talk about a stock we currently own, we will make it known that we own it.

This email is authorised by Anthony Khighneston Authorised Representative Number zero zero 1 2 9 2 7 1 8 of M F & Co. Asset Management Proprietary Limited (A F S L five 2 zero 4 4 2). No part of this content may be reproduced in [00:49:00] any form without the prior consent of Spacecraft Publishing.

Here’s an update on the performance of the other stocks we’ve done as a pulled pork (deep dive) since the start of the show. Average return so far is 40%.

0 Comments